Money

Beyond your bank balance: 5 numbers you should know by 50

Most of us can be irrational about our personal finances as retirement fears take over - will you have enough? How much do you even need? Fear not: getting a grip on these 5 numbers can save your sanity and sort your future in one fell swoop.

By Alex Brooks

Hitting the age of 50 means entering the ‘pre-retirement’ financial phase of life – it’s time to get real about money.

There’s still a 10-year investment horizon before we reach 60 and can access our superannuation and 17 years before we hit 67 and may be entitled to receive the Age Pension.

That’s plenty of time to start practising responsible financial adulting, right? Knowing the following 5 personal finance numbers will help you get there:

1. INCOME: cash flowing keeps dreams growing

The first and most obvious number to know is your income.

You need to know how much money you receive in any given year, month or week (whatever period of time works best for you).

Income can include wages or salary, net income from a business, dividends or profits from investments, interest from the bank, government payments, and any other positive money gains you receive.

The really important part of understanding this number is working out whether you can begin to:

- Build out multiple streams of income so you can become less reliant on a primary wage or salary in the future.

- Sock more money away to save or invest for future income (see number 4)

Find your most recent income statements in the Australian Tax Office Services online services.

2. SPENDING: categorise and strategise

Spending falls into 2 categories: essential and non-essential.

Essentials are the big things you need to live each month – housing, bills, groceries and transport.

Non-essential spending includes the lifestyle expenses you can reign in – things like new clothes, eating out at restaurants and subscription services.

Most bank apps now let you categorise your spending. Call your bank to find out the easiest and fastest way to do it. Here’s how the big four banks do it:

- CommBank category budgets

- Westpac budget tools

- NAB spending tracking

- ANZ Your Money Report and app features

The old-school way to identify your spending means printing out the last 3 to 6 months of bank statements, grabbing 2 highlighters, and going through each transaction line by line.

Use one colour to highlight essential spending and the other for discretionary buys.

Make a copy of Citro’s spending tracker and personalise it with your spending habits to help work out where your money is going.

MoneySmart’s budget planner tool may also be helpful. Keeping tabs on your average monthly and annual spending will be a vital part of how you plan to retire later on, so why not start now?

3. DEBT: a termite that eats away financial freedom

How much money do you owe and to whom?

Understanding debt is the first step to managing it. List all your debts by total value, interest, payment due dates and any other obligations.

‘Bad’ debt is the type that ultimately costs you more money over time – things like credit cards, car loans or lines of credit are best extinguished as quickly as possible.

Read 7 ways to reduce debt. Then if you are still struggling with debt, call the National Debt Helpline to access free financial counselling services.

Good debt, such as a mortgage that will ultimately buy you a home to live in rent-free, can be paid off over longer periods of time.

A mortgage-free home – regardless of whether it is worth $400,000 or $4 million – is considered exempt from the Age Pension assets test and is usually a vital pillar of financial stability in retirement.

A home that’s your main residence is also capital gains tax-free, which means you can sell it later on to downsize and put some of the proceeds into your superannuation or other investments.

4. SAVINGS RATE: this determines future wealth

Your savings rate is the percentage of your income that you can save in any given week, month or year.

This rate is a measure of your wealth relative to your living expenses. The higher your savings rate today; the more wealth you will likely have relative to your expenses in the future.

Now that you know your income and spending habits, how much of your income can you put away to save, invest or pay down debt?

There are 3 ways to increase your savings rate:

- Reduce your spending while maintaining your current income.

- Increase your income while maintaining your current spending.

- Simultaneously increase your income and reduce your spending (the fast track).

Let’s start with reducing your spending.

The best way to do this is to decide whether you can cut down your big 4 costs, which are housing, transport, bills and food. Making cuts to the big 4 can mean making major changes to your day-to-day lifestyle, which is why plenty of people choose never to do it.

If that’s you, you can maintain your current spending but still increase your saving rate by increasing your income.

An easy way to choose this route is to treat ‘extra’ money as though it doesn’t really exist – so save those tax cuts, put your end-of-year bonus in a savings account or squirrel away any tax refunds before you can spend them.

Other options to increase your income while maintaining your current spending include:

- Starting a side hustle or business (which requires investing more of your time).

- Asking for a wage rise or seeking a better-paying promotion in your existing job.

- Investing inside or outside of your superannuation for future income in the long term. Ask your boss if they will consider salary packaging or allowing you to make pre-tax superannuation contributions.

Of course, the third way to increase your savings rate is to do all of the above. Simultaneously reducing your spending and increasing your income is the fast-track way to reach your financial goals.

Understanding your overall ‘net worth’ can help you play with your savings rate and how you achieve it.

Use MoneySmart’s net worth calculator to help assess your current financial position. Use your net worth to track your progress from year to year and stay on top of your financial situation to make informed decisions about your future.

5. SUPER STASH: find your retirement number

How much do you need to live on when you no longer want to rely on wages or business income?

This question is as individual as the clothes we wear, the partner we choose and the car we drive. It will also come down to where you live and whether you own your own home.

It’s the amount of money you need in your superannuation (or investments outside of super) – in addition to owning your home outright – to comfortably hang up your work boots and financially retire.

A lot of people panic right here, convinced they can never afford to retire. But, of course, that’s very rarely the case.

Australia has the safety net of the Age Pension, which people can apply for after they reach 67. There is also a Work Bonus, concession cards and other benefits to help people as they get older. All of these things combine with your super and other investments to make up your income in retirement.

The first part of finding your retirement number is working out how much you have in superannuation today. You can find this out by:

- Finding your most recent superannuation statement (don’t forget to keep your logins secure and regularly check your super to make sure everything is being paid correctly).

- Logging into MyGov or ATO online services and doing a super health check.

You can then use a range of online tools to estimate how much superannuation you’ll have in the future by:

- Calling your superannuation fund and asking them which online tools they recommend to help you work this out. Some funds also offer free help – sometimes called general advice – to project how much you’ll need to retire.

- Using a comprehensive online retirement income calculator, like this one.

- Playing with MoneySmart’s retirement planner calculator and superannuation calculator.

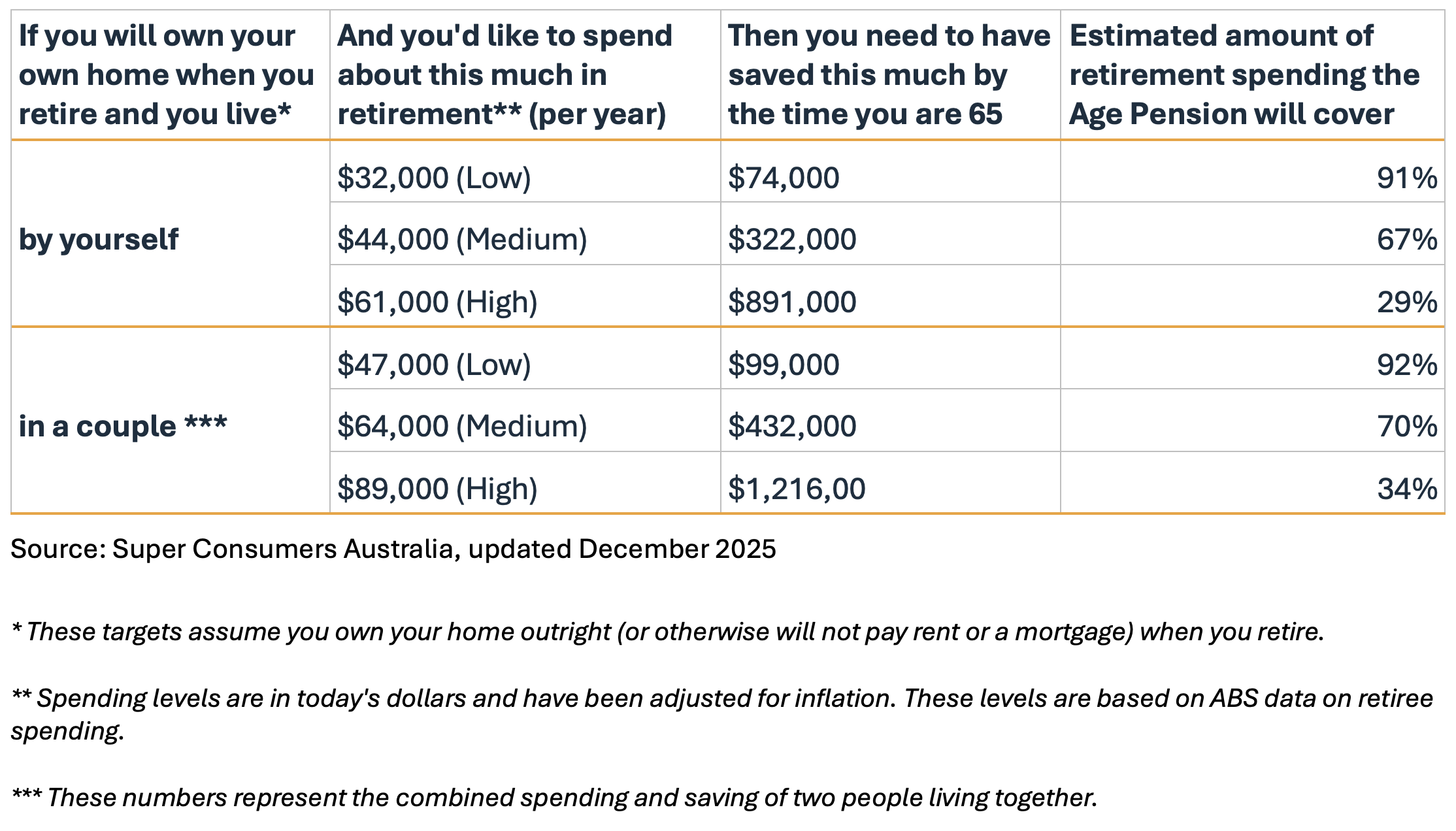

Super Consumers Australia publishes retirement savings targets for pre-retirees aged 55 to 59, to offer general guidance on how to nail your retirement number.

ASFA – the Association of Superannuation Funds of Australia – also publishes the Retirement Standard that outlines how much people need to fund a modest or comfortable retirement.

Working out how much you’ll need before you can retire involves a confluence of decisions like:

- How much you spend each year.

- Where you want to live (could you move somewhere cheaper?).

- How much you want to travel versus enjoy the simple things in life.

- What memberships, hobbies and subscriptions you enjoy.

- Whether you want to factor in top private health insurance or aged care costs.

- How much you want to help your children with gifts or loans or buying a house.

- What government benefits you might be entitled to.

Sometimes it’s worth paying a financial advisor to help you make these decisions. For other people, continuing to work or taking advantage of their super early in retirement (something we’ve nicknamed Peak Pension) might be the way to go.

It’s different strokes for different folks. Whatever choices you make, the sooner you nail your 5 numbers, the easier it will be.

Advice given in this article is general in nature and does not take into account your personal circumstances. It is not intended to influence readers' decisions about investing or financial products. They should always seek their own professional advice that takes into account their own personal circumstances before making any financial decisions.

You might also like: